The American Electricity Crisis

Disseminated on behalf of SolarBank Corporation.

The American power grid is entering one of the most consequential turning points in modern history.

Record-breaking demand, driven by transformative shifts in technology, industry, and climate policy, is colliding with aging infrastructure and long-standing regulatory bottlenecks.

AI data centers, electric vehicles, and clean energy mandates are fueling an electricity consumption boom not seen in decades… forcing a fundamental reevaluation of how the nation generates, distributes, and manages power.

Against this backdrop, policymakers, utilities, developers, and regulators are scrambling to adapt. Federal and state-level agendas are pulling in different directions.

Legacy fossil fuel systems are not sustainable in the long run, while renewables and batteries struggle to scale fast enough. At the same time, households and businesses are grappling with higher utility costs, and grid operators are warning of tightening reserve margins across several regions.

This complex landscape is unfolding in real time, shaped by a surge of investment, legislation, innovation, and constraint which is all converging to define the next era of U.S. electricity.

As the United States enters a new era of rapid technological advancement and economic realignment, its energy system is facing unprecedented pressure. The explosive growth of artificial intelligence, widespread adoption of electric vehicles, a revival in domestic manufacturing, and aggressive decarbonization goals are all converging to dramatically increase electricity demand across the country.

From federal energy policy shifts and rising utility costs to regional grid bottlenecks and the evolving mix of generation sources, it examines the multi-layered challenges and responses taking shape across the public and private sectors.

Federal Policy and Regulatory Developments

The United States is facing a historic surge in electricity demand, driven by AI data centers, electric vehicles (EVs), industrial reshoring, and the broader electrification of homes and businesses. This spike has prompted significant federal attention across administrations.

The Biden administration previously committed over $8 billion to grid upgrades, supporting over 100 transmission projects through grants and loan guarantees.

As of early 2025, many of these projects were still underway, particularly in rural areas needing new high-voltage lines to connect renewable energy.

The Trump administration, which began in January 2025, has shifted priorities. While it rolled back major elements of Biden’s climate agenda and launched reviews of the Inflation Reduction Act and 2021 infrastructure law, it has simultaneously pledged to fast-track permitting for energy infrastructure, including pipelines and transmission lines.

President Trump has openly criticized wind energy but acknowledged that a modern grid is essential for scaling America’s data and AI economy.

Tensions continue between the reliability needs of the grid and emissions targets. The EPA’s 2024 proposed carbon rules would require coal plants to install carbon capture technology by 2032 and limit emissions from new gas plants.

Grid operators and utility executives argue these rules could jeopardize reliability by forcing early closures of firm power sources. The North American Electric Reliability Corporation (NERC) has warned Congress that these mandates threaten stability during a period of rising demand.

The Federal Energy Regulatory Commission (FERC) has focused on clearing interconnection backlogs and improving long-term transmission planning.

Analysts, including from Wood Mackenzie, highlight that meeting new demand in a decarbonized way is the nation’s largest energy challenge in decades.

State-Level Initiatives and Grid Expansion

Texas

Texas is arguably ground zero for the U.S. electricity crunch. The state’s main grid operator, ERCOT, now projects nearly a doubling of demand by 2030. The growth stems from rapid population increases and energy-intensive industries such as semiconductor manufacturing, cryptocurrency mining, and AI data centers.

In response, Texas lawmakers created the Texas Energy Fund in 2023 with $5 billion in low-interest loans for gas plant construction.

By early 2025, that fund had been doubled to $10 billion. The state has also invested in weatherizing infrastructure, vegetation management, and grid resiliency. Officials are now calling for an urgent review of all policies affecting capacity and reliability.

California

California faces its own electricity surge due to aggressive electrification policies. Mandates for all new car sales to be electric by 2035 and decarbonizing buildings have driven up projected load. The California Independent System Operator (CAISO) expects electricity demand to rise sharply through the 2030s.

To mitigate peak demand, California has invested heavily in demand response programs, with over 500 MW now enrolled. It’s also exploring vehicle-to-grid policies and has extended the lifespan of its Diablo Canyon nuclear plant to retain steady baseload power.

Wildfires, heatwaves, and droughts have compounded the grid’s vulnerabilities, prompting billions in infrastructure upgrades and distributed energy programs.

Among the companies stepping into this opportunity is SolarBank Corporation (NASDAQ:SUUN), a renewable energy developer with an expanding presence across the U.S. market.

The company focuses on behind-the-meter and community solar installations, and is now also integrating battery storage solutions. These offerings align closely with California’s broader push for decentralized energy infrastructure and greater grid flexibility in response to climate-driven volatility and demand growth.

As of Q1 2025, SolarBank (NASDAQ:SUUN) has completed over 100 projects across North America and currently has more than 1GW of projects in its development pipeline, including 15 MW in development in California alone.

Other States

States across the Midwest and Northeast have passed clean energy mandates targeting 100% carbon-free electricity between 2040 and 2045. This has spurred wind, solar, and battery deployment.

However, many states like West Virginia and Wyoming are now reconsidering nuclear energy and lifting construction bans to pursue small modular reactors.

Meanwhile, the Southeast continues to expand gas and nuclear generation, with Georgia’s new Vogtle Units 3 and 4 now online.

Electricity Tariffs, Utility Bills, and Regulatory Shifts

Average retail electricity prices rose about 28% from 2019 to 2024, reaching nearly $0.18/kWh. Average monthly household utility bills are approaching $300.

In 2023 alone, over $10 billion in rate hikes were approved by state regulators, which more than doubled the previous year. These hikes funded wildfire prevention, infrastructure upgrades, and generation to meet rising demand.

Utilities are increasingly adopting time-of-use (TOU) rates and demand charges, especially in California, Colorado, and New York.

These structures encourage off-peak usage and attempt to smooth peak load curves exacerbated by EVs and air conditioning. Net metering revisions, such as California’s NEM 3.0, reduce compensation for excess rooftop solar energy, prompting a pivot toward solar-plus-storage systems.

Energy affordability is becoming a political flashpoint. One in six American households now faces energy poverty. Consumer advocates are calling for targeted relief programs, while others are advocating for reforms to utility profit models and more federal investment to avoid overburdening ratepayers.

Energy Sources: Under Pressure and Expansion

Natural Gas

Natural gas remains the primary backup to intermittent renewables. In 2024, GE Vernova’s gas turbine orders doubled, and U.S. gas-fired generation hit record highs.

While gas ensures reliability, critics warn it could undermine climate goals due to carbon and methane emissions. Nonetheless, utilities continue to invest in peaker plants as a short-term reliability solution.

Coal

Coal is seeing a temporary reprieve in some regions. Plants previously scheduled for retirement are being extended by 1–2 years to maintain reserve margins.

U.S. coal generation is expected to rise slightly (~6%) in 2025 due to elevated gas prices but is still on a long-term decline. New coal capacity is virtually nonexistent, and most plants are expected to shut down by 2040.

Renewables

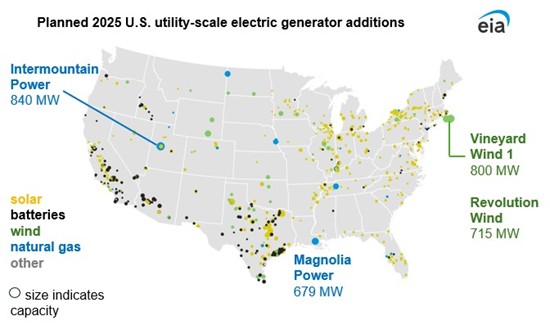

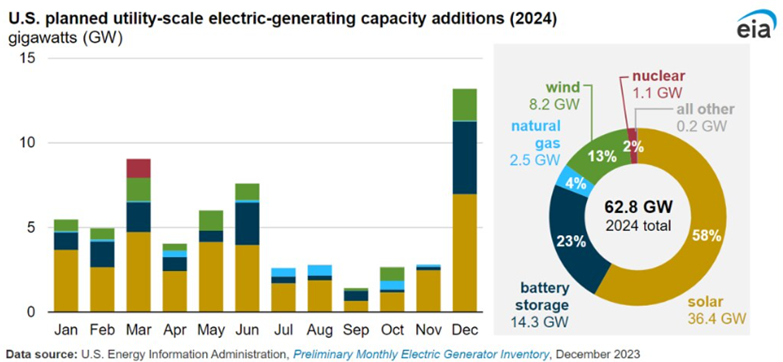

Solar and wind are expanding rapidly. Utility-scale solar installations reached 36.4 GW in 2024.

Over 2.5 TW of renewable projects are in interconnection queues, but permitting and transmission constraints delay many from being built.

While the Trump administration is launching a review, while it remains in force the Inflation Reduction Act continues to supercharge investment through tax credits.

SolarBank (NASDAQ:SUUN) is also expanding its footprint within the U.S. utility and community-scale solar sector. The company has active development efforts in key solar growth states like New York, and Pennsylvania, which are regions benefiting from aggressive clean energy mandates and incentive structures.

Having secured participation in multiple state-backed community solar programs and maintaining a pipeline exceeding 1 GW of renewable energy projects, SolarBank’s strategic focus on high-demand zones and emphasis on pairing solar with storage positions it as a responsive developer in addressing both energy reliability and decarbonization needs.

Wind power continues to grow, particularly in the Midwest and Plains, though local opposition and supply chain delays affect timelines.

Offshore wind is beginning to scale on the East Coast, with the first commercial farms due online by late 2025.

Battery Storage

Battery storage is essential for integrating renewables. Over 10 GW of storage was added in 2024, and 2025 is on track for 18.2 GW, which is an all-time record. These batteries help shift solar generation into evening hours and provide emergency backup.

While most are lithium-ion with 1–4 hour durations, longer-duration storage technologies are under development. One notable player in this space is SolarBank (SUUN), which continues to expand its solar-plus-storage projects across the U.S., focusing on municipal, commercial, and industrial customers.

Their model integrates turnkey development and asset management, allowing fast deployment in states with aggressive clean energy targets like New York.

As of March 2025, SolarBank has 60 MWH of solar-plus-storage capacity under development across North America and is targeting 100 MWH in completed capacity by the end of 2025.

Its U.S. project pipeline includes community solar installations in New York, where the company has success in obtaining community solar subscribers, as supported by Solar Simplified.

Nuclear

The successful startup of Vogtle Units 3 and 4 added 2.2 GW of carbon-free baseload power.

Existing nuclear plants are receiving license extensions up to 80 years, with states like Illinois and New Jersey offering subsidies to prevent early shutdowns. Interest in small modular reactors is growing, with projects proposed in Wyoming, Wisconsin, and Idaho.

Emerging Technology Demands

AI and Data Centers

Data center electricity usage is projected to double by 2028, rising from 176 TWh in 2023 to 325–580 TWh. This is driven by AI workloads requiring massive parallel computations.

Northern Virginia, Texas, and Utah are hotspots for data center expansion. Dominion Energy has fast-tracked substations, and federal agencies are easing siting regulations for AI-related infrastructure.

Electric Vehicles

EVs consumed about 18 TWh in 2023 and are expected to exceed 130 TWh by 2030. Utilities are rolling out EV-specific tariffs and demand-side management tools.

California alone expects 5 million EVs by 2030. Vehicle-to-grid programs could eventually enable EVs to serve as distributed storage, helping stabilize the grid.

Cryptocurrency and Industry

Crypto mining remains a significant electricity user, particularly in Texas and Kentucky. Mining firms participate in demand response programs, curtailing usage during peak periods.

Industrial expansion, particularly in battery manufacturing and semiconductor fabs, is also lifting demand in places like Ohio, Michigan, and Arizona.

Grid Stability and Infrastructure Challenges

Peak Demand and Weather

U.S. power demand hit a record 744 GW during the July 2024 heatwave. Most regions avoided blackouts, but operators remain on edge. Texas surpassed 85,000 MW multiple times in summer 2024, narrowly avoiding outages thanks to emergency generation and demand response.

Wildfires in California, ice storms in the Midwest, and hurricanes along the Gulf Coast are increasingly disrupting power infrastructure. In response, utilities are burying lines, hardening substations, and deploying microgrids in vulnerable areas.

Infrastructure Upgrades

Grid spending by U.S. utilities is at an all-time high, with over $12.7 billion in pending rate cases for infrastructure enhancements. Transmission projects connecting wind and solar generation to population centers are under construction nationwide.

The Department of Energy is funding storm-hardening programs and advanced grid control technologies.

FERC has proposed rules to improve capacity markets and ensure sufficient firm generation. NERC is updating reliability standards, including for cybersecurity and cold-weather readiness. Demand response participation also reached record levels in 2024.

Outlook and Upcoming Events

The EIA projects U.S. electricity consumption will hit new records in both 2024 and 2025, growing ~2–3% annually.

Summer 2025 could see another all-time peak, especially if an El Niño year brings extreme heat.

Key developments to watch include:

- Finalization of EPA power plant emissions rules

- Potential revisions to the Inflation Reduction Act

- FERC’s upcoming transmission planning reforms

- DOE’s Electric Grid Summit in mid-2025

- Completion of offshore wind projects and new battery installations

- Continued buildout of EV charging infrastructure

- NERC’s 2025 Summer Reliability Assessment (May)

These initiatives will shape the reliability, affordability, and sustainability of the U.S. power system through the end of the decade.

📌 Investor Note

The U.S. electricity landscape is undergoing one of the most significant structural transformations in decades. Demand for power is accelerating at a pace not seen since the industrial expansion of the mid-20th century.

Unlike past cycles, today’s growth is being driven by foundational shifts: artificial intelligence infrastructure, EV fleets, digital manufacturing, electrified heating, and industrial reshoring. This is not a cyclical bump. It’s a generational transition.

Electricity is quickly becoming the lifeblood of America’s economic reinvention, and the grid is under growing strain. At the same time, the energy system is being rebuilt in real time.

Utility-scale solar, battery storage, microgrids, small modular nuclear, and distributed generation are all expanding, but they’re not yet doing so fast enough to meet the surge in demand. Constraints in permitting, interconnection, and transmission continue to delay capacity additions even as billions in public and private capital chase opportunities.

For investors, this presents a moment of both opportunity and asymmetry. Established utility players are burdened with slow-moving regulatory frameworks and rate case cycles.

Meanwhile, newer entrants with flexible models (especially those focused on community solar, storage integration, and municipal or C&I power) are gaining ground.

Companies like SolarBank (NASDAQ: SUUN), for example, are actively growing portfolios in high-demand states like New York and California by targeting shovel-ready solar-plus-storage projects tied to state-level clean energy mandates.

These firms are often earlier in their lifecycle, which can hold the potential for outperformance as grid needs outpace legacy supply.

Investors should also be watching which states are aggressively incentivizing clean energy deployment through direct funding, utility offtake guarantees, and expedited permitting, especially where those incentives align with structural demand growth from data centers, EV infrastructure, or industrial expansion.

Texas, Illinois, California, and New York are particularly active, with billions earmarked for grid modernization and localized capacity additions.

There’s also growing momentum around vertical integration. Developers that can manage engineering, procurement, construction, and long-term asset ownership are often better positioned to secure incentives, control costs, and generate recurring revenue through power purchase agreements. Some are even building merchant or hybrid merchant-regulated business models to capture pricing arbitrage as capacity tightens.

Over the next 24 to 36 months, expect significant capital inflows into distributed energy, behind-the-meter solutions, and mid-scale storage tied to community or commercial users.

The Inflation Reduction Act (assuming it remains in force) and various state clean energy laws will continue to shape winners and losers. Those who can execute quickly and navigate policy complexity are likely to lead.

Ultimately, the grid transition is not theoretical. The opportunities for equity growth exist not just in utilities or big wind/solar manufacturers, but in agile developers, storage integrators, and companies addressing grid flexibility at the edge.

This is where unmet demand is becoming visible, and where returns may be realized ahead of broad market recognition.

Sources:

U.S. Energy Information Administration (EIA) – Solar, battery storage to lead new U.S. generating capacity additions: https://www.eia.gov/todayinenergy/detail.php?id=54559

U.S. Energy Information Administration (EIA) – U.S. power use to reach record highs in 2024 and 2025: https://www.eia.gov/todayinenergy/detail.php?id=55986

Federal Energy Regulatory Commission (FERC) – Winter Energy Market and Reliability Assessment 2024–2025: https://www.ferc.gov/media/winter-2024-25-energy-market-and-reliability-assessment

North American Electric Reliability Corporation (NERC) – Long-Term Reliability Assessment 2024: https://www.nerc.com/pa/RAPA/ra/Reliability%20Assessments%20DL/NERC_LTRA_2024.pdf

U.S. DOE Grid Deployment Office – Grid resilience and innovation partnerships: https://www.energy.gov/gdo/grid-resilience-and-innovation-partnerships-program

Bloomberg – AI’s growing power needs reshape the U.S. grid: https://www.bloomberg.com/news/articles/2024-11-18/ai-data-centers-are-rewiring-the-us-power-grid

Reuters – U.S. power demand to reach record highs in 2024, 2025: https://www.reuters.com/business/energy/us-power-use-reach-record-highs-2024-2025-eia-forecast-says-2024-12-10/

Reuters – Innovators prime creaky US power grid to lift higher loads: https://www.reuters.com/markets/commodities/innovators-prime-creaky-us-power-grid-lift-higher-loads-maguire-2025-03-18/

Utility Dive – 2025 US power sector outlook: https://www.utilitydive.com/news/2025-electric-utility-trends-outlook-2025/738845/

Utility Dive – Solar expected to be top source of new US generation through 2025: https://www.utilitydive.com/news/solar-lead-electricity-generation-growth-2025-eia/704340/

Wall Street Journal – Hunger for Electricity Seen Keeping Renewable-Power Investment Flowing Under Trump: https://www.wsj.com/articles/hunger-for-electricity-seen-keeping-renewable-power-investment-flowing-under-trump-b7e7c616

Politico – EPA’s new power plant rules could affect U.S. grid reliability: https://www.politico.com/news/2024/09/22/epa-carbon-capture-rule-coal-plants-00117394

SolarBank Corporation (NASDAQ: SUUN) – Investor presentation Q1 2025: https://solarbankcorp.com/investors/

CAISO – 2024-2025 Transmission Plan and Forecast: https://www.caiso.com/Documents/2024CaliforniaISOTransmissionPlan.pdf

ERCOT – ERCOT Planning and Forecasting 2024: https://www.ercot.com/mpm/planning

NYISO – Power Trends 2024: https://www.nyiso.com/documents/20142/2223020/2024-Power-Trends-Report.pdf

Greentech Media – Utility-scale battery growth surges in U.S. markets: https://www.greentechmedia.com/articles/read/record-utility-scale-battery-growth-in-2024

Canary Media – Solar and storage trends across North America: https://www.canarymedia.com/articles/solar/solar-and-storage-trends-across-north-america

Disclaimer:

This report is intended for informational and educational purposes only and does not constitute financial, investment, or trading advice. The content herein is based on publicly available data believed to be accurate as of the stated publication date. No representation or warranty, express or implied, is made as to the completeness or accuracy of the information presented. The authors and publishers of this report are not registered investment advisors and shall not be held liable for any decisions made or actions taken based on the information provided. All investments carry risk. You should conduct your own due diligence and consult a licensed financial advisor before making any investment decisions.

There are several risks associated with the development of the projects detailed in this report. The development of any project is subject to the continued availability of third-party financing arrangements for the project owners and the risks associated with the construction of a solar project. There is no certainty the projects disclosed in this report will be completed on schedule or that they will operate in accordance with their design capacity. In addition, governments may revise, reduce or eliminate incentives and policy support schemes for solar power, which could result in future projects no longer being economic.

You should read and understand this disclaimer in its entirety before joining the website or clicking any links from the publisher of this email (the “Publisher”). The information (collectively the “Advertisement”) disseminated by email, text or other method by the Publisher including this publication is a paid commercial advertisement and should not be relied upon for making an investment decision or any other purpose. The Publisher is engaged in the business of marketing and advertising the securities of publicly traded companies in exchange for compensation. The track record, gains, upside, and/or losses mentioned in the Advertisement, if any, should not be considered as true or accurate or be the basis for an investment. The Publisher does not verify the accuracy or completeness of any information included in the Advertisement.

The Advertisement is not a solicitation or recommendation to buy securities of the advertised company. An offer to buy or sell securities can be made only by a disclosure document that complies with applicable securities laws and only in the states or other jurisdictions in which the security is eligible for sale. The Advertisement is not a disclosure document. The Advertisement is only a favorable snapshot of unverified information about the advertised company. An investor considering purchasing the securities should always do so only with the assistance of his legal, tax and investment advisors. Investors should review with his or her investment advisor, tax advisor or attorney, if and to the extent available, any information concerning a potential investment at the web sites of the U.S. Securities and Exchange Commission (the “SEC”) at www.sec.gov; the Financial Industry Regulatory Authority (the “FINRA”) at www.FINRA.org, and relevant State Securities Administrator website and the OTC Markets website at www.otcmarkets.com. The Publisher cautions investors to read the SEC advisory to investors concerning Internet Stock Fraud at www.sec.gov/consumer/cyberfr.html , as well as related information published by the FINRA on how to invest carefully. Investors are responsible for verifying all information in the Advertisement. As an advertiser, we do not verify any information we publish. The Advertisement should not be considered true or complete.

The Publisher does not offer investment advice or analysis, and the Publisher further urges you to consult your own independent tax, business, financial and investment advisors concerning any investment you make in securities particularly those quoted on the OTC Markets. Investing in securities is highly speculative and carries an extremely high degree of risk. You could lose your entire investment if you invest in any company mentioned in the Advertisement. You acknowledge that we are not an investment advisory service, a broker-dealer or an investment adviser and we are not qualified to act as such. You acknowledge that you will consult with your own independent, tax, financial and/or legal advisers regarding any decisions as to any company mentioned here. We have not determined if the Advertisement is accurate, correct or truthful. The Advertisement is compiled from publicly available information, which includes, but is not limited to, no cost online research, magazines, newspapers, reports filed with the SEC or information furnished by way of press releases.

Owners and operators of the Publisher have been compensated up to $15,000 for the distribution of this advertisement. The Publisher and its owners and operators hold no stocks or bonds in companies discussed in the Advertisement.

By accepting the Advertisement, you agree and acknowledge that any hyperlinks to the website of (1) a client company, (2) the party issuing or preparing the information for the company, or (3) other information contained in the Advertisement is provided only for your reference and convenience. The advertiser is not responsible for the accuracy or reliability of these external sites, nor is it responsible for the content, opinions, products or other materials on external sites or information sources. If you use, act upon or make decisions in reliance on information contained in any disseminated report/release or any hyperlink, you do so at your own risk and agree to hold us, our officers, directors, shareholders, affiliates and agents harmless. You acknowledge that you are not relying on the Publisher, and we are not liable for any actions taken by you based on any information contained in any disseminated email or hyperlink.