Understanding the Difference Between APR vs. APY

When it comes to borrowing or saving money, understanding the difference between APR (Annual Percentage Rate) and APY (Annual Percentage Yield) is crucial. These two financial terms may sound similar, but they have distinct meanings and implications for consumers. In this comprehensive guide, we will delve into what APR and APY are, how they differ, and why they matter to your financial well-being.

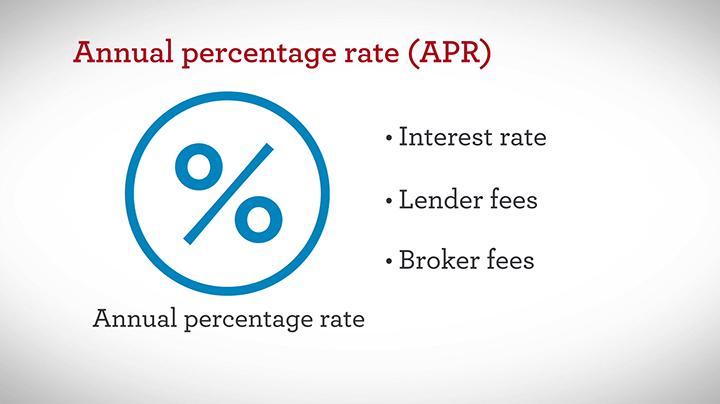

What is APR?

APR stands for Annual Percentage Rate, and it represents the annual cost of borrowing money. When you take out a loan or credit card, the APR is the interest rate you will pay on the outstanding balance. It includes both the interest rate and any fees or charges associated with the loan. APR is expressed as a percentage and helps consumers understand the total cost of borrowing over a year.

What is APY?

APY stands for Annual Percentage Yield, and it represents the annual rate of return on savings or investment accounts. APY takes into account the interest rate, compounding frequency, and any fees or charges associated with the account. It shows how much your money will grow over a year, including the effect of compounding interest. APY is also expressed as a percentage and helps consumers compare the growth potential of different savings accounts or investment products.

Key Differences Between APR and APY

1. Calculation Method:

- APR: The APR calculation does not take compounding into account. It is a straightforward annual interest rate that does not consider how often interest is added to the balance.

- APY: The APY calculation considers compounding, which means interest is added to the principal balance, and future interest is earned on that new total. This leads to higher returns compared to simple interest calculation.

2. Use Cases:

- APR: APR is primarily used for borrowing money, such as mortgages, car loans, or credit cards. It helps consumers understand the true cost of borrowing and compare different loan options.

- APY: APY is used for savings accounts, certificates of deposit (CDs), and other investment products. It shows how much your initial investment will grow over time, taking into account compounding interest.

3. Comparison Factor:

- APR: When comparing loan offers, lower APRs indicate cheaper borrowing costs. However, it’s essential to consider the terms of the loan, including fees and repayment schedule.

- APY: When comparing savings or investment accounts, higher APYs indicate greater growth potential for your money. Look for accounts with competitive APYs and favorable terms to maximize your savings.

The Importance of Understanding APR vs. APY

Understanding the difference between APR and APY is crucial for making informed financial decisions. Whether you are borrowing money or saving for the future, these two metrics can impact your bottom line. Here are some key reasons why APR and APY matter:

Benefits and Practical Tips:

- By knowing the APR of a loan, you can compare different borrowing options and choose the one with the lowest cost.

- Understanding the APY of a savings account can help you maximize your returns and achieve your financial goals faster.

- Being aware of the difference between APR and APY can prevent costly mistakes and ensure you make sound financial choices.

Case Studies:

- Case Study 1:

John is comparing two credit card offers. Card A has an APR of 15%, while Card B has an APR of 18%. By choosing Card A, John can save money on interest payments.

- Case Study 2:

Sarah wants to open a savings account to grow her emergency fund. Bank A offers an APY of 1.5%, while Bank B offers an APY of 2%. By choosing Bank B, Sarah can earn more interest on her savings over time.

First-hand Experience:

- Personal Finance Tip:

When taking out a loan, always read the fine print and understand the APR, including any fees or charges involved. Look for loans with low APRs to save money on interest payments.

- Investment Strategy:

When investing in a savings account or CD, consider the APY and compounding frequency to maximize your returns. Regularly monitor your accounts and explore higher APY options to grow your savings faster.

Conclusion

In conclusion, APR and APY are essential financial metrics that play a significant role in borrowing and saving money. By understanding the difference between APR and APY, consumers can make informed decisions that benefit their financial well-being. Whether you are taking out a loan or opening a savings account, knowing how APR and APY work can help you save money, earn more interest, and achieve your financial goals. Keep these key differences in mind when navigating the world of personal finance, and make smart choices that align with your financial objectives.